The Australian Taxation Office (ATO) has significantly restricted its view on tax deductions for taxpayers who own holiday homes or investment properties leased for short-term stays.

The Denial of Holding Cost Deductions

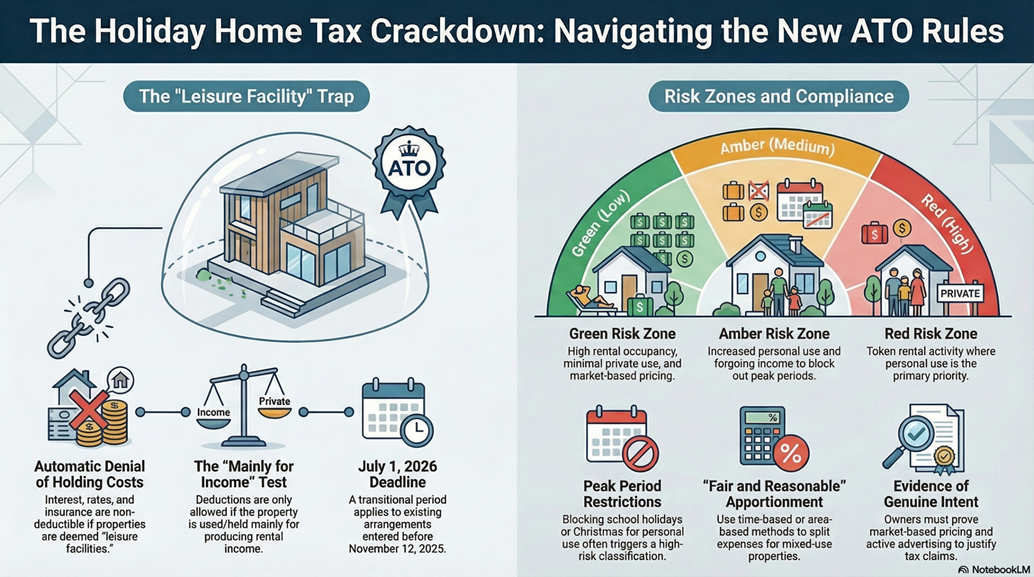

The most critical change is that if a property is classified as a leisure facility, owners will be denied deductions for property holding costs, such as mortgage interest, council rates, land tax, and insurance. To maintain these deductions, you must now prove the property is used “mainly” to produce assessable rental income.

The “Mainly” Test and Peak Periods

The ATO is moving away from simply counting the number of days a property is available for rent. Instead, they will take a nuanced approach that prioritises genuine availability during peak seasons. Blocking out peak weeks (such as Christmas, Easter, or school holidays) for personal use is a major “red flag” that may trigger the denial of all major deductions. If the property is only available during off-peak periods when there is little demand, the ATO may conclude it is held primarily for private recreation.

What Remains Deductible?

Even if some deductions are restricted, costs directly tied to earning rental income remain deductible to the extent the property was actually rented.

These include:

- Advertising fees and platform commissions.

- Cleaning costs and agent commissions related to a rental.

- Direct maintenance costs incurred for the rental period.

The ATO Risk Framework

The ATO has introduced a risk-based compliance framework to help owners assess their situation:

- Green (Low Risk): The property is mostly rented with minimal private use.

- Amber (Medium Risk): Increased personal use or forgoing income to make the property available for family during peak times.

- Red (High Risk): Primarily personal use with limited or token rental activity.

Record-Keeping is Essential

To claim any deductions safely, you must maintain records. This includes detailed logs of rental versus private use, evidence of market-based pricing, copies of advertisements, and booking confirmations. Any ad hoc or “unrealistic” apportionment methods for mixed-use expenses are likely to be disallowed.

Transitional Period

While these rules apply to expenses from 12 November 2025, the ATO has offered a grace period. They will not devote compliance resources to reviewing these specific issues for expenses incurred before 1 July 2026, provided the rental arrangement was entered into before 12 November 2025.

We strongly recommend reviewing your holiday home arrangements now to ensure they align with these stricter standards.