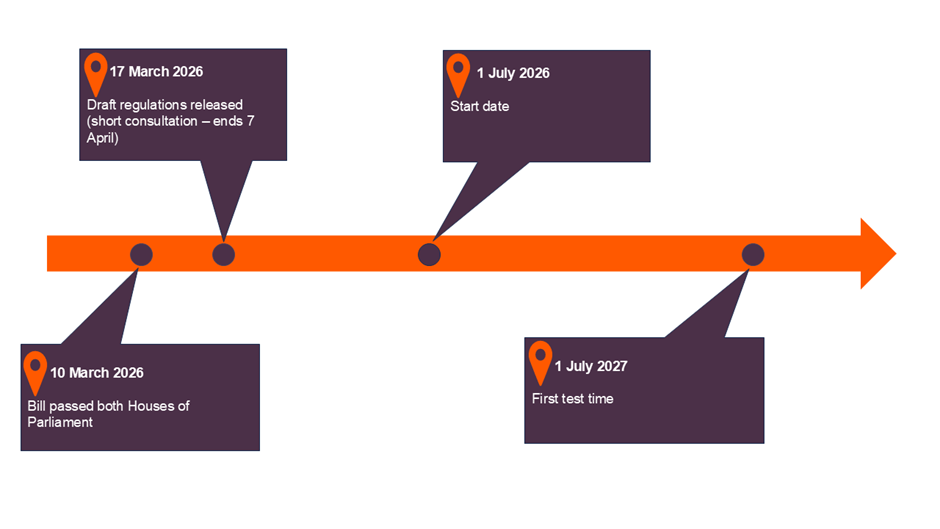

Since our earlier update outlining the proposed Division 296 measures (Read: Proposed Division 296 Changes: What You Need to Know – Harris Black), the Federal Government passed the legislation on 17th March 2026. The Treasury Laws Amendment (Building a Stronger and Fairer Super System) Bill 2026 has cleared both houses of Parliament and received Royal Assent, locking in a new tax regime for individuals with large superannuation balances.

The finalised Division 296 framework confirms a two‑tiered additional tax on realised superannuation earnings, replacing earlier proposals that included unrealised gains.

Division 296 tax will be calculated per member as follows:

- 15% x proportion of superannuation balance over $3 million (“large super balance threshold”) x relevant superannuation earnings; plus

- 10% x proportion of superannuation balance over $10 million (“very large super balance threshold”) x relevant superannuation earnings.

When Will It Apply?

The new rules will commence 1 July 2026, with the first assessments expected on lodgement of the 2026–27 financial year annual return.

Contact your Harris Black team member for more details these changes to Division 296.